And now in more (not so) good news on the economic front, Zillow is suggesting that there may be a looming “double-dip” in home values.

At least from Seattle’s perspective, we’re not listed as one of most likely candidates for another drop in value, but data from Zillow’s Home Value Index indicates if you bought anytime in the last few years, your home is probably worth less than when you bought it.

Here’s a chart showing the change in values over the last five years.

According to Zillow, here are some toplevel findings:

- Decreasing Home Values: Home values changed -5.8% to a Zillow Home Value Index of $300,400. Values also fell in the short-term, changing -0.5% from November to December. The Zillow Home Value Index measures the value of all homes, not just those that sold in a particular period.

- Homes with Negative equity: 22 percent of all owners of single-family homes with mortgages were underwater at the end of Q4.

- Foreclosure re-sales: 19.5 percent of all sales in December were foreclosure re-sales (REO sales). Nationally, foreclosure re-sales made up 20.3 percent of all sales.

- Homes sold for a loss: 18.5% of all homes sold in December sold for a loss.

I’m not a real estate analyst, so I’ll point to the SeattlePI for more information.

Here’s a look at values over the past 10 years in the same neighborhoods:

Here’s the full press release:

Continued High Negative Equity and Home Value Declines

Put a Damper on an Encouraging 2009

Despite Some Areas Experiencing Flattening or Reversal of Home Value Declines Last Year,

One in Five Markets Now Showing Signs of a Possible Double Dip in Home Values,

According to Q4 2009 Zillow® Real Estate Market Reports

Key facts:

Negative equity remains high at 21 percent of all single family homes with mortgages, but was flat quarter-over-quarter.

U.S. home values fell 5 percent year-over-year, and declined 0.5 percent quarter-over-quarter, marking the 12th consecutive quarter of year-over-year declines.

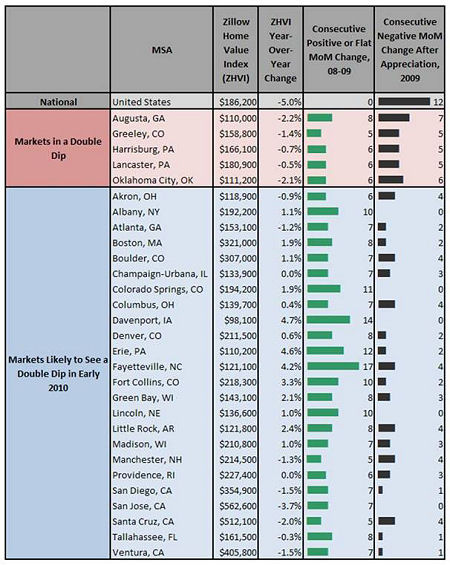

In one in five, or 29 of the 143 markets tracked by Zillow, home values have flattened or have begun to decrease again after showing at least five consecutive monthly increases during 2009 – early signs of a what could become a “double dip.”

SEATTLE – Feb. 10, 2010 — Home values across the country declined again in the fourth quarter of 2009, as the Zillow Home Value Index[i] fell 5 percent year-over-year, and -0.5 percent quarter-over-quarter, to $186,200. That marked the 12th consecutive quarter of year-over-year declines, according to the fourth quarter Zillow Real Estate Market Reports.

Despite home value declines seen across most of the country throughout 2009, some markets experienced what appeared to be a bottom in home value declines, or even increases in home values during the year. However, the fourth quarter of the year brought signs that the fledgling recovery of home values in many of these markets is slowing again. If the declines are sustained, the result will be a “double dip[iii]” in home values, defined as two periods of sustained declines in home values separated by a brief period of stabilization or recovery.

One in five, or 29 of the 143 markets tracked by Zillow, showed at least five consecutive month-over-month increases in home values during 2009 before beginning to flatten or fall again in the second part of the year. These markets include the Boston metropolitan statistical area (MSA), the Atlanta MSA and the San Diego MSA.

Home values in an additional 29 markets, including the Los Angeles and New York MSAs, increased on a month-over-month basis each month throughout the fourth quarter. However, the rate of increase slowed from November to December in 21 of those markets, and several appear likely to experience several months of sustained decline in early 2010.

The percent of single family homes with mortgages in negative equity was essentially flat from the third to the fourth quarter, changing from 21 percent in Q3 to 21.4 percent in Q4. This comes after a decrease in negative equity from the second quarter’s 23 percent.

The number of homeowners losing their homes to foreclosure[iv] across the country reached a peak in December, with more than one in every thousand homes being foreclosed – a number not reached since Zillow began recording national foreclosure data in 2000.

“While we have seen strong stabilization in home values during 2009, there are clear signs that they will turn more negative in the near-term,” said Zillow Chief Economist Stan Humphries. “What we saw in mid-2009 was a brief respite from a larger market correction that has not yet run its course. The good news is that, for those markets that will see a double dip in home values before reaching a definitive bottom, this second dip will not be a return to the magnitude of depreciation seen earlier, but rather will look more like a modest aftershock of the earlier downturn.

“The recent stabilization owed a lot to policy support in the form of tax credits, lower interest rates and increased Federal Housing Administration lending. The remaining correction in home values we’ll see in the first half of this year is a function of market fundamentals, such as the increasing flow of foreclosures, high levels of inventory in the market and a probable decrease in demand as the impact of the tax credit wanes and mortgage rates rise. While the next few months are likely to bring further home value declines in most markets, we do expect to see a national bottom in home prices by the middle of this year. Thereafter, home values are likely to bounce along the bottom with real appreciation remaining negligible for some time.”

Foreclosure re-sales[v] across the country remained high, making up more than one-fifth (20.3 percent) of all U.S. home sales in December. Foreclosure re-sales also made up the majority of sales in several MSAs, including

the Merced, Calif. MSA (68.3 percent), the Las Vegas MSA (64 percent) and the Modesto, Calif. MSA (62 percent). Additionally, 28.5 percent of home sales nationwide sold for less than what the seller originally paid.

Several markets across the country showed positive longer-term appreciation. Home values increased year-over-year in 27 of 143 markets and remained flat in 15.

The Boston MSA was the largest area with year-over-year appreciation, despite its more recent downturn in home values. The area’s Zillow Home Value Index rose 1.9 percent in 2009. Home values in the Boston area rose for eight months in 2009, which outweighed the recent declines.

Markets in Double Dip/Markets Showing Signs of Impending Double Dip

The full national report, in its interactive format, is available at www.zillow.com/local-info on Wednesday, Feb. 10. Additionally, in most areas data is available at the state, metro, county, city, ZIP and neighborhood level.

About Zillow.com®

Zillow.com is an online real estate marketplace where homeowners, buyers, sellers, renters, real estate agents and mortgage professionals find and share vital information about homes and mortgages. Launched in early 2006 with Zestimate® home values and data on millions of U.S. homes, Zillow has since added homes for sale and homes for rent, a directory of real estate and lending professionals, Zillow Advice and Zillow Mortgage Marketplace. One of the most-visited U.S. real estate Web sites, with more than eight million unique visitors per month, Zillow’s goal is to help people become smarter about homes and real estate in every stage of their lives — home buying, selling, renting, remodeling and financing. The company is headquartered in Seattle and has raised $87 million in funding.

Zillow.com, Zillow and Zestimate are registered trademarks of Zillow, Inc.

[i] The Zillow Home Value Index is the median Zestimate valuation for a given geographic area on a given day and includes the value of all single-family residences, condominiums and cooperatives, regardless of whether they sold within a given period. The Home Value Index at the national level is calculated using a weighted average of the median home value for each county and includes data from 440 metropolitan statistical areas. It is expressed in dollars and is for a particular geographic region.

[ii] The data in Zillow’s Real Estate Market Reports is aggregated from public sources by a number of data providers for 143 Metropolitan Statistical Areas dating back to 1996. Mortgage and home loan data is typically recorded in each county and publicly available through a county recorder’s office.

[iii] A market is defined as having a double-dip in home values if the following four conditions are met: 1) The market experiences five or more consecutive months of monthly home value depreciation and the annualized depreciation rate over this period is greater than 1 percent; 2) prior to this period described in (1), the market experienced five or more consecutive months of monthly home value appreciation and the annualized appreciation rate over this period was greater than 1%; 3) prior to this period described in (2), the market experienced five or more consecutive months of monthly home value depreciation and the annualized depreciation rate over this period was greater than 1%; and 4) the time span from the peak between (1) and (2) and the trough between (2) and (3) is 12 months or less.

[iv] Foreclosures are defined as a Trustee’s Deed Upon Sale or equivalent transaction.

[v] Foreclosure re-sales capture mostly sales of bank-owned (REO) homes. It measures sales of homes that were foreclosed on in the previous 12 months.